As the conflict between Iran, the United States, and Israel witnesses escalation after escalation, worries over the magnitude of global economic consequences have emerged. As was the case in past military conflicts affecting the region, the centrality of the Gulf to the global energy system means that military disruptions are likely to translate into economic spillovers via globally interconnected energy. While sharp rises in energy prices, interruptions to trade, and financial market volatility have been observed so far, the scale of economic impacts will largely be determined by the scope and duration of the war.

Prior to the beginning of the conflict in late February 2026, the economic picture in many parts of the world remained relatively weak in comparison with past metrics of economic growth and inflation. The inflationary shock that began with pandemic-related supply disruptions and was later intensified by the Russia-Ukraine war had begun to ease, but consumers and investors in many parts of the world remained affected by high energy costs, food prices that had not returned to normal levels, and persistently high interest rates.

Disruptions to Energy Markets – Price Spike or Longer-term Impact?

Hostilities have brought shipping through the Strait of Hormuz, through which approximately 20 percent of the world’s crude oil and liquified natural gas transit, to an almost complete standstill. Energy markets responded almost immediately, with global benchmark Brent crude passing US$100/barrel on 7th March, an increase of over 50 percent over the last month and around 30 percent on a year-on-year basis. Showing the magnitude of the current geopolitical risk premium, prior to the conflict, energy analysts assessed a Brent price of around US$60-65/barrel according to normal supply-demand conditions.

The present oil market situation is more pessimistic than that experienced during the 12-day war between Israel and Iran in June 2025, which saw Brent crude spiking above US$80/barrel before returning to levels of approximately US$67-70/barrel by the end of the month. Indeed, the rapid return in June to fundamentals-driven crude oil price levels was largely attributable to market relief over a short-duration conflict with highly circumscribed objectives and limited disruptions to energy production and transport. With Brent crude prices crossing US$100/barrel on 7 March and with European natural gas futures breaching €50/MWh (Figure 1), the military and energy market scenario is significantly more severe.

It remains unclear whether current oil prices are a short-term spike or whether the situation will give rise to a more prolonged global energy price shock and associated inflationary trend. Strikes on Qatar’s LNG production facilities, Saudi Arabia’s Ras Tanura refinery, and collapsing Iraqi crude production raise serious concerns about damage to Gulf oil and gas infrastructure. Upward price pressure can also be expected to result as Asian oil traders begin to search for alternative crude oil cargoes. Moreover, a further complicating factor has recently emerged: the current lack of exports through the Strait of Hormuz means that crude oil storage tanks are gradually becoming full, and that this will necessitate reducing oil production within a matter of a few weeks. Major production shutdowns, if they occur, will most likely add to upward oil price pressures.

The situation in gas markets is similar but remains—in relative terms—well short of price reactions seen in the past; European gas prices reached €322 per megawatt hour shortly after Russia’s invasion of Ukraine in 2022, compared with current levels of around €50 per megawatt hour.

Figure 1: Brent Crude Oil and Natural Gas Prices (Dec 2025–Mar 2026)

Source: EIA (Brent crude); ICE exchange London (Dutch TTF NG Futures).

Mitigants and Policy Responses – Enough to Avoid a Global Energy Shock?

Several mitigants and policy responses are being deployed in attempts to avert a severe global oil price shock. Recent days have seen discussions focus on additional production as well as on the release of non-Gulf emergency oil stocks. The OPEC+ group of countries has agreed to add additional production of 200,000 barrels per day to supplies beginning in April; however, these volumes are modest because of the inherently limited spare production capacity of non-Gulf OPEC producers. More significantly, G7 finance ministers are discussing bringing emergency oil reserves to market in an effort to address the current price surge.[1] The joint emergency reserves of International Energy Agency (IEA) members total approximately 1.2 billion barrels, and the Financial Times reports that a release of 25-30 percent (around 300–400 million barrels) of total reserves is being considered for release.

The major component of these emergency reserves—the U.S. Strategic Petroleum Reserve (SPR) currently holds 415 million barrels of crude oil—can gradually be sold into oil markets to mitigate oil prices.[2] The SPR was last employed for this purpose in 2022 after sanctions were imposed on Russian energy at the beginning of the Russia-Ukraine conflict. At that time, the release of an additional 180 million barrels from the SPR over six months stabilized disruptions to oil markets, reduced U.S. gasoline prices, and mitigated the inflationary effect of rising energy costs. However, with a typical selling rate of ~1 million barrels per day, the SPR on its own, while useful to loosen supply in oil markets, will be insufficient. Substantial contributions will also be required from other major IEA members, including Japan, Germany, France, Italy, and the U.K. to slow price increases while the Strait of Hormuz remains effectively closed. While the release of emergency stocks will calm energy markets, volumes will be insufficient to replace exports shipped through Hormuz for any meaningful period of time.

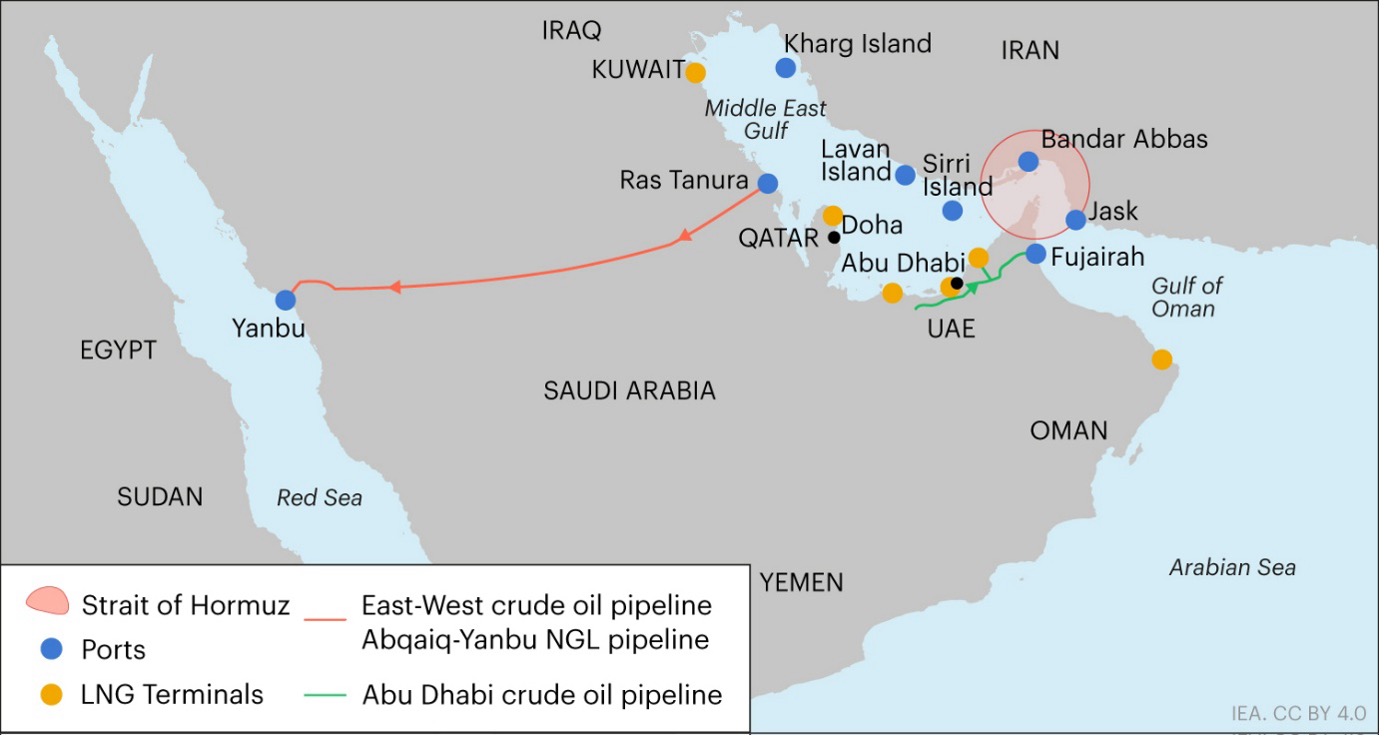

Figure 2: Alternative Crude Oil Pipelines Bypassing Strait of Hormuz

Source: International Energy Agency (IEA), https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

A second approach involves maximizing throughput of the two crude oil pipelines (Figure 2) that bypass the Strait of Hormuz. Saudi Arabia’s 1,200-kilometer East-West pipeline transports crude from its Eastern oil fields to the Red Sea Port of Yanbu, while the UAE’s 370-kilometer-long Habshan-Fujairah pipeline runs from Abu Dhabi’s Habshan field to Fujairah port on the Gulf of Oman. These strategically significant alternative routes are, however, constrained by capacity limitations; the UAE’s pipeline is able to move 1.5 million barrels per day of crude to the port of Fujairah, while Saudi Arabia’s East-West pipeline to Yanbu on the Red Sea operates at a capacity of 5 million barrels per day. Excluding refined products (which account for around 4-5 million barrels per day), crude oil shipments through Hormuz amount to approximately 15-16 million barrels per day. Both pipelines operating at full capacity would nonetheless leave around 10 million barrels per day to be exported by sea, subject to closure of the Strait of Hormuz.

While some of the mechanisms set out above, i.e., alternative routes for oil exports and the gradual release of non-Gulf emergency stocks, can have a moderating effect on brief price spikes, large and persistent price spikes in energy prices are considerably harder to stabilize. Depending on the duration and extent of the conflict, should oil prices remain at or near US$100/barrel for more than a few weeks, the energy price shock will almost inevitably transmit into economies.

Asian Reliance on Energy Exports Transiting Hormuz

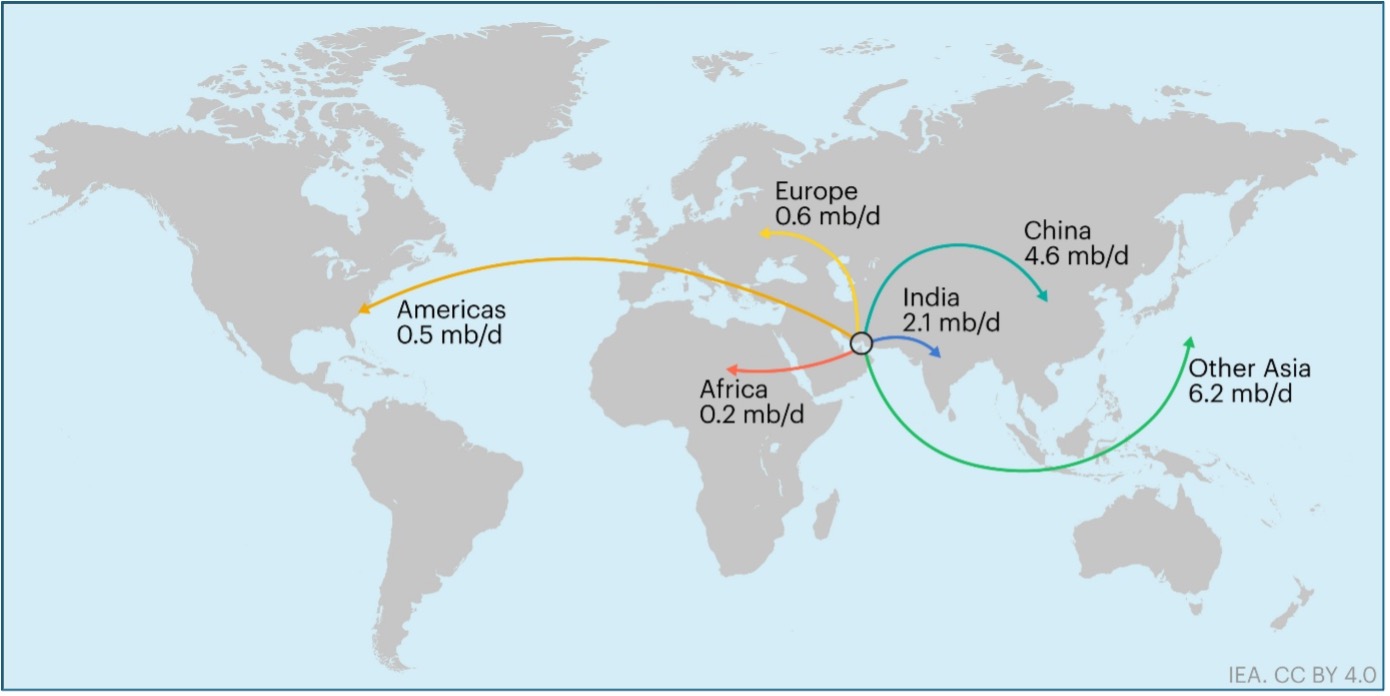

In the short- to medium-term, the energy-importing regions of Asia are vulnerable to energy shocks from the conflict. Asia’s exposure to its energy exports transiting Hormuz is outsized, with over 80% of both crude oil and LNG cargoes estimated to be bound for Asian markets in 2024. Among Asian nations, China and India alone imported 44% of Gulf crude oil in 2025, with only 4% of Gulf crude oil exports received by Europe (Figure 3). Recognizing the risks of an energy supply squeeze for India’s economy, on 5 March, the U.S. granted India a 30-day waiver on the purchase of Russian crude oil. China is reported to have accumulated a reserve of 1.3 billion barrels of crude oil, but has nonetheless ordered a suspension of diesel and petrol exports.[3] Reduced supplies to refineries and petrochemical plants in Asia dependent on Gulf Crude may eventually result in the invocation of force majeure contractual clauses helping corporates avoid liability due to conflict.

Figure 3: Crude Oil Exports Transiting the Strait of Hormuz by Destination (2025)

Source: International Energy Agency (IEA), https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

The strategic importance for Asia of unencumbered transit through Hormuz isn’t limited to crude oil: closure imperils the flow of LNG cargoes critical to Asian economies and energy security. Approximately 83 percent of LNG cargoes transiting the Strait of Hormuz in 2024 were shipped to Asian markets, with China, India, and South Korea the top destinations, accounting for 52 percent of all Hormuz LNG flows that year.[4] Qatar’s LNG exports account for approximately 20% of global gas shipped by sea. Almost all of Pakistan’s LNG imports, three quarters of the imports of Bangladesh, and almost half of India’s gas imports are Gulf LNG. This concentration in gas supply and transport explains why the 3 March announcement by QatarEnergy that LNG production from its North Field reservoir was halted as a result of strikes on Ras Laffan and Mesaieed Industrial Cities immediately sent gas prices in European and Asian gas markets sharply upwards.

Equity markets in Asian energy-importing countries quickly responded to the escalating crisis, with the MSCI Asia-Pacific index declining by 2-3 percent, Indonesian and Taiwanese indices falling by 3-4 percent, Thailand’s SET 50 index closing with a drop of more than 8 percent, and the South Korean KOSPI index crashing by over 12 percent on 4 March.

The halt to LNG shipments through the Strait of Hormuz is, in market terms, equally if not more alarming than the interruption of crude shipments. Halting production of Qatar’s Ras Laffan facility on 2 March effectively removed around 75 million tons of LNG per year, equivalent to 17 percent of global exports.[5] Unlike in the case of crude oil, suppliers of LNG have not yet developed alternative pipeline routes or strategic storage comparable to the U.S. Strategic Petroleum Reserve, meaning that without this buffering capacity, supply shocks will quickly transfer to markets and consumers.[6]

Rising European Energy Prices and the Spectre of Resurgent Inflation

To date, European gas prices have been similarly affected, with prices surging by almost 50% as a result of a stop in Qatari LNG production due to Iranian strikes on its energy infrastructure.[7] While Europe is less dependent on oil and LNG transiting Hormuz than China, India, Japan or South Korea, it is nonetheless exposed through price surges of global LNG spot prices for cargoes. Signs of increasing competition between Europe and Asia are already emerging, with at least one LNG cargo originally bound for France rerouting towards Asia.[8]

This price competition arrives at a poor time for the continent: the especially cold 2025–2026 winter has impacted EU gas stocks, which might need to be replenished before next winter at high prices if current disruptions persist. Moreover, since the Ukraine-Russia conflict in 2022, Europe has had to compensate for reducing imports of Russian pipeline gas by importing large—and much more expensive—volumes of LNG cargoes from the U.S., Norway, and Qatar. This unavoidable substitution in energy supply has placed Europe in a position of having to absorb higher energy costs to power industry. Given the importance of industry and manufacturing to EU economies, the energy price increase has effectively undermined the continent’s manufacturing competitiveness, global export position and economic outlook. Among European nations, Germany and Italy remain particularly exposed to LNG imports.

European worries may extend further to concerns that rising energy prices will feed into an inflationary spiral. Eurozone inflation is expected to be 1.9% in February, a significant jump from January’s level of 1.7%.[9] These inflation levels, which are already close to the European Central Bank’s 2% target and were collected prior to the current conflict, suggest that monetary policy action by the ECB might be a possibility in the near future. Europe’s exposure to a potentially serious energy shock has started to affect currency markets, with the euro’s weakening position against the dollar reflecting fears that the conflict could renew EU inflation scenarios from late 2022 until mid-2023.

Should oil prices remain elevated for weeks or months, energy prices will channel into economies via higher transport, electricity, and manufacturing costs, rising household energy expenditures, and lower industrial output. In turn, as was the case during the early stage of the Russia-Ukraine war, central banks may be forced, yet again, to sharply increase interest rates with predictable results for economic growth, consumer spending and real disposable incomes. In 2022, as a result of the energy price shock following Russia’s invasion of Ukraine, the EU experienced a deficit of 0.8 percent in euro area GDP compared with a surplus of 2.8 percent in 2021.[10]

The overall economic picture emerging now for Europe is developing the character of a potential energy price shock that may well trigger a resurgence in inflation, loss of economic growth momentum, and a weakening in the continent’s competitiveness as a global exporter. Optimism for a quick resolution of the war since its beginning on 28th February is fading. Should oil prices remain above US$100/barrel for a period of several weeks or months, high energy costs will gradually become embedded in the economies of vulnerable regions and countries.

[1] Financial Times, “G7 to discuss joint release of emergency oil reserves,” Financial Times, 2026, https://www.ft.com/content/e1141f96-db3e-41ef-b978-0131e91f1d82.

[2] U.S. Department of Energy, “Strategic Petroleum Reserve,” March 5, 2026, https://www.energy.gov/hgeo/opr/strategic-petroleum-reserve.

[3] “The Iran War Has Put Asia on the Brink of an Energy Panic,” The Economist, March 8, 2026, https://www.economist.com/finance-and-economics/2026/03/08/the-iran-war-has-put-asia-on-the-brink-of-an-energy-panic.

[4] U.S. Energy Information Administration, “About One-Fifth of Global Liquefied Natural Gas Trade Flows through the Strait of Hormuz,” Today in Energy, June 24, 2025, https://www.eia.gov/todayinenergy/detail.php?id=65584.

[5] “The Nightmare Iran Energy Scenario Is Becoming Reality,” The Economist, March 3, 2026, https://www.economist.com/finance-and-economics/2026/03/03/the-nightmare-iran-energy-scenario-is-becoming-reality.

[6] Camilla Palladino, “Hormuz Crisis Is a Wake-Up Call for Complacent Gas Consumers,” Financial Times, March 2, 2026, https://www.ft.com/content/0bd22934-e4ee-4d8f-b874-582c884c9c30.

[7] “European Gas Extends Gains With Uncertainty Over Qatar LNG Halt,” Bloomberg, March 3, 2026, https://www.bloomberg.com/news/articles/2026-03-03/european-gas-extends-gains-with-uncertainty-over-qatar-lng-halt.

[8] “Europe Confronts Threat of Another Energy Crisis,” Financial Times, March 5, 2026, https://www.ft.com/content/d48f6a08-0b7d-4a01-a84f-b0fbecf03915.

[9] Doloresz Katanich, “Eurozone Inflation Sees Unexpected Rise: Is the Worst Yet to Come?” Euronews, March 3, 2026, https://www.euronews.com/business/2026/03/03/eurozone-inflation-sees-unexpected-rise-is-the-worst-yet-to-come.

[10] Lorenz Emter, Michael Fidora, Fausto Pastoris, Martin Schmitz, Jerzy Niemczyk, and Mykola Ryzhenkov, “The Euro Area Current Account After the Pandemic and Energy Shock,” Economic Bulletin, Issue 6 (Frankfurt: European Central Bank, 2023), https://www.ecb.europa.eu/press/economic-bulletin/articles/2023/html/ecb.ebart202306_01~4cd4215076.en.html?